Do I Have to Pay UKSL Debt Collection? Avoid Harassment

By

Janine

Janine Marsh

Financial Expert

My name’s Janine, and I’m a mum of two who’s always been passionate about trying to cut down spending costs. I am now sharing as much financial knowledge as I possibly can to help your money go that little bit further.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Powered by MoneyNerd, featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

If you’re dealing with a UKSL Debt Collection notice, you might be feeling worried. You’re not alone. Every month, more than 12,000 people visit here looking for guidance on debt matters.

In this guide, we’ll explore:

Who is UKSL Debt Collection and if they are real.

Why UKSL might get in touch with you.

How to handle the letter from UKSL Debt.

What UKSL Debt Collection can legally do.

What help is there in the UK for debt.

Having debt can be hard. We know this because some of us have been in the same spot. We’ve faced debt and the struggle of not knowing the next step, which means we have the knowledge to assist you. Let’s dive in and learn more about dealing with UKSL Debt Collection.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Why would UKSL contact you?

UKSL will contact you to recover a debt owed to another company such as a utility provider. When you fall behind or miss payments to a utility company, chances are they have instructed UKSL Debt to recover the amount.

That said, a utility company will have sent many letters reminding you of an outstanding bill beforehand. UKSL Debt gets involved when the amount remains unpaid!

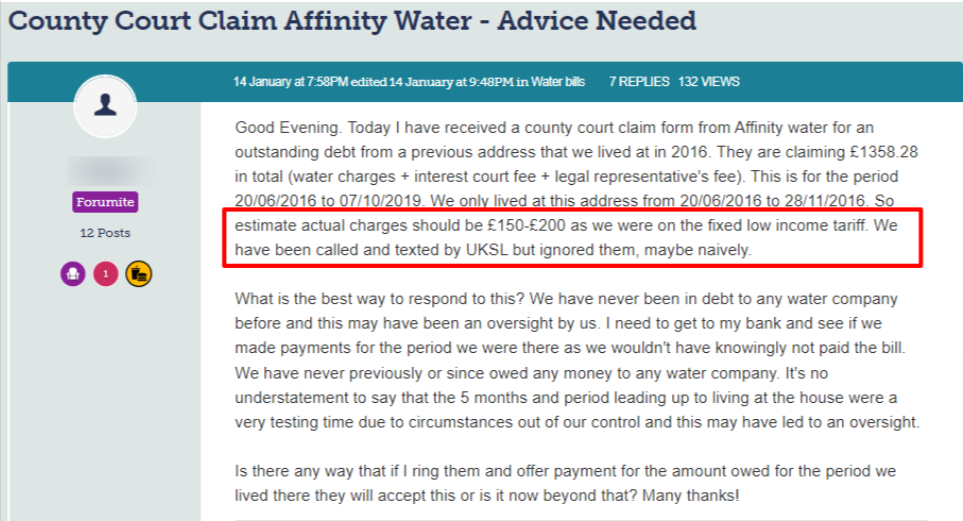

Whatever you do, don’t ignore UKSL correspondence. Take a look at what happened to one unfortunate person:

As mentioned, you may have to pay UKSL Debt if they can prove the debt is yours. Don’t accept a verbal confirmation from the debt collection agency. They must provide you with ‘hard’ proof you owe the money!

You may not have to pay if UKSL can’t prove the debt is yours.

Next, establish the debt is still current and not statute-barred. You may not have to pay if it’s at least six years old and meets all the criteria listed above.

You have the right to tell UKSL to stop contacting you if the debt isn’t yours and the statute barred.

Debt collectors cannot continue to harass you and if they do, they’re acting unlawfully.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

In short, it’s better to remain in contact with UKSL and negotiate an affordable payment plan with them. But only once the debt collector has proved the debt is yours and it’s not statute-barred!

UKSL must follow a Code of Practice that dictates what debt collectors can and cannot lawfully do when they contact you.

A debt collector can legally:

Ask you to pay them directly

Contact you and visit you at your home

Discuss a debt with you politely and discreetly

A debt collector cannot lawfully do:

Force entry into a home

Clamp vehicles or seize possessions

Discuss a debt with family members, friends, employers or neighbours which breaches privacy laws

Make out they are Enforcement Agents (bailiffs) which is a criminal offence

Imply they have court-issued documents

Talk in confusing terms using legal jargon

Apply pressure to take out another loan to pay a debt

You have the right to report a debt collector if you feel they are intimidating you or harassing you. But first, file a complaint with their head office. You can then lodge a complaint with the Financial Ombudsman Service (FOS).

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

It’s hard to remain calm and think clearly when you get a letter from UKSL Debt. But it’s important not to panic and to deal with the problem sooner rather than later.

First, check what the debt is for and if you really owe the money. You can do this by writing back to UKSL Debt asking them to ‘prove’ the debt is yours. A debt collection agency must respect this request.

Send the letter by registered post and keep a copy of the letter for your own records.

Next, check how old the debt is. Why? Because debts which are at least six years old are statute barred. In short, a debt that is old is unenforceable! However, the debt still exists and could impact your credit rating. But you won’t get a CCJ if the limitation period has expired.

That said, there are criteria that must be met for a debt to be statute barred which I’ve listed here:

You’ve not been in contact with the credit for six years

You’ve paid nothing towards clearing the debt for six years

There are no existing court proceedings to recover the debt

How do you contact UKSL Debt Collection?

I’ve put together UKSL Debt Collection’s contact details here:

Unit 4 Gander LaneBarlborough, Chesterfield Derbyshire, England, S43 4PZ

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

My name’s Janine, and I’m a mum of two who’s always been passionate about trying to cut down spending costs. I am now sharing as much financial knowledge as I possibly can to help your money go that little bit further.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.