I’m Receiving Debt Collection Letters for Someone Else? (Answer)

By

Janine

Janine Marsh

Financial Expert

My name’s Janine, and I’m a mum of two who’s always been passionate about trying to cut down spending costs. I am now sharing as much financial knowledge as I possibly can to help your money go that little bit further.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Powered by MoneyNerd, featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Dealing with debt is tough, but getting letters about someone else’s debt can be confusing and worrying. You’re not alone on this path. Every month, over 12,000 people visit this site seeking guidance on debt issues.

In this article, we’ll answer your questions:

Do you need to pay debt collectors?

How can you clear a debt that’s not yours?

Can you lower your repayments?

How to get an incorrect credit report removed?

How to handle being chased for a debt that’s not yours?

We understand your stress; our team has dealt with these issues before. Don’t worry; we’ve got the knowledge to guide you.

Ready to learn more about managing debt that isn’t yours? Let’s dive in!

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

First, is the debt yours?

Debt collection agencies and creditors get things wrong. They fail to update their systems with debtors’ current addresses! Moreover, they use automated systems so letters are sent out automatically to an address the debtor no longer lives at!

So, here’s what to do when you get debt collection letters for someone else:

Go through all the details on the debt letterEstablish whether you entered into a joint credit agreement

Check you didn’t act as a guarantor for someone else

Ask the sender to ‘prove’ you owe the money and that the debt is yours to make sure you actually owe any money!

Can you clear a debt that’s not yours?

Mistakes happen whether clerical or other, so yes you can clear a debt that’s not yours. If you believe the debt isn’t yours or your name is on the letter in error, make sure you let the sender know.

Go through your credit file by contacting a credit reference agency. This will tell you whether you have any defaults, missed payments or CCJs against you!

If the debt is on your credit history but it’s definitely not yours, you can ask for it to be removed. Contact the credit reference agency and request they correct the information.

How a debt solution could help

Some debt solutions can:

Stop nasty calls from creditors

Freeze interest and charges

Reduce your monthly

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

Monthly income

£2,504

Monthly expenses

£2,345

Total debt

£32,049

Monthly debt repayments

Before

£587

After

£158

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

If the creditor/debt collection agency still insists on contacting you, write a letter of complaint and send it to their head office. Make sure you send the letter by registered post.

If you ignore things, you could be missing out on sorting a bad situation out once and for all! Moreover, chances are you’d get more annoying letters delivered to your address.

Plus, the creditor or debt collection agency could win a case in court. The result? Even if the debt isn’t yours, enforcement officers (bailiffs) could visit you at home!

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Don’t let enforcement officers (bailiffs) into your home if they show up over a debt that’s not yours. Instead, talk to them through a slightly opened window or your letterbox!

You could opt to talk to the bailiffs outside your home but make sure you put a distance between them and your property!

Show them a utility invoice or council tax bill to make them go away if necessary! If a bailiff refuses to leave, file a complaint with their head office then lodge a complaint with the Financial Ombudsman Services!

An enforcement officer (bailiff) must leave when you ask them to. Moreover, they have no legal right to clamp your vehicle or seize any of your possession over a debt that’s not yours!

How do I get an incorrect credit report removed?

File a dispute with the credit reporting company when you identify an incorrect entry on your credit file. For example, this could be with Experian, TransUnion or Equifax. Write a letter telling them what is wrong and provide proof to support the dispute.

What can you do when chased for a debt that’s not yours?

You could get a letter about a debt belonging to someone else when someone fails to update their details with creditors. It’s an annoying situation you need to resolve sooner rather than later!

The way to deal with the situation is to cross out the name on the envelope and write ‘not known at this address’ across it. Post the letter back to the sender. It’s a free service so you don’t have to pay!

This should stop the sender from bothering you again. However, they may get in touch again asking you to provide more information.

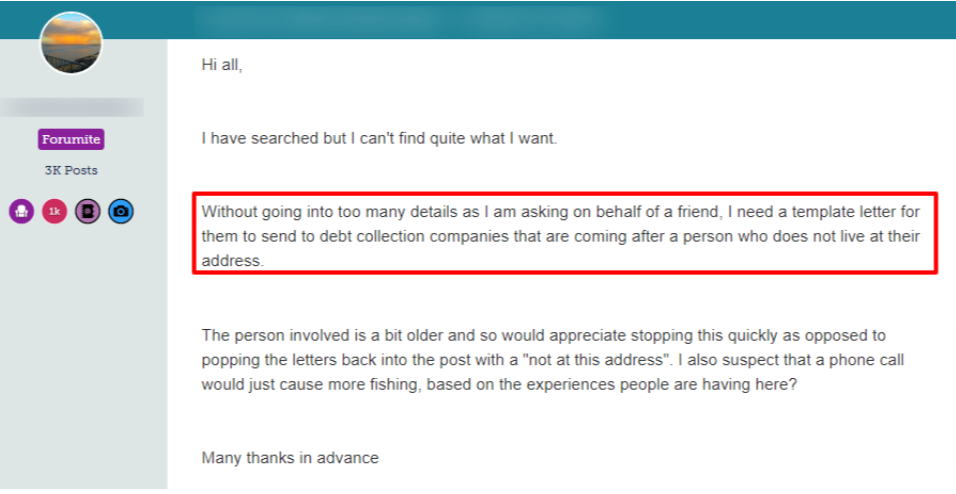

Check out what one unfortunate person asked on a forum:

You have no legal obligation to provide any further information to a creditor or debt collection agency! But it could help stop them from getting in touch again. So, for example, send them a copy of a council tax bill to get them off your back.

What if the debt is proven to be yours?

You’d have to deal with the creditor or debt collector if it turns out you were the guarantor for someone else. In this instance, you may be liable for the money owed.

It happens when the creditor/debt collection agency hasn’t been able to catch up with the real debtor!

Moreover, when you have a joint credit agreement with someone, you’d be liable for paying what’s owed too!

Who can you complain to?

You can file a complaint if you’re being harassed by a creditor or debt collection agency over a debt that’s not yours. You should:

Step 1

File a complaint with a financial services firm

Step 2

Lodge a complaint with the Financial Ombudsman Services

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

My name’s Janine, and I’m a mum of two who’s always been passionate about trying to cut down spending costs. I am now sharing as much financial knowledge as I possibly can to help your money go that little bit further.

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.