How Does an IVA Restrict Your Spending?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Our article, ‘How Does an IVA Restrict Your Spending?’ is here to help you understand the workings of an IVA.

Each month, over 12,000 people visit our site for guidance on topics like this; you’re not alone.

We know it can be concerning when you’re unsure how to pay a debt or what might happen if you can’t pay. Don’t worry! In this article, we’ll explain:

- What an IVA is and how it works

- How an IVA can affect your spending

- What expenses you can have during an IVA

- What happens if your income changes

- Other options you have to tackle your debt

Our team knows how tough it can be to navigate the world of debt solutions; some of us have been in your shoes. We’re here to help you understand IVAs and how they restrict your spending.

How does an IVA restrict your spending?

An IVA restricts your spending because your IP will make an IVA proposal to creditors that makes you pay your disposable income into the IVA. You will be forced to live on a tight budget.

The IP will ensure you have enough money to keep up with essential living costs (your expenses), but your surplus money is to be used to pay into the IVA. This prevents you from making luxury purchases for a long time.

Therefore, using an IVA requires you to budget accurately and effectively.

What expenses are allowed in an IVA?

You’re allowed to include all expenses that are considered essential to maintain essential living standards and to ensure you remain employed. Examples include your rent, utility bills, groceries, standard hygiene products and costs you incur to get to and from work.

When creating your IVA proposal, you will have fixed and variable IVA expenses.

Fixed expenses are those that stay the same each week or month, such as rent payments. Whereas variable IVA expenses are those that can change more frequently, such as fuel costs you might incur as part of your job.

Variable expenses can be challenged if they don’t match up with what these expenses usually cost. But each IVA is taken on its own merit. For example, your work commute costs might be more expensive due to living in a certain area and travelling further to work than the average person does.

You might have an emergency fund calculated into your expenses. This is money that you’re expected to put aside in the event of an emergency, such as needing to replace a washing machine.

Can you have disposable income with an IVA?

Your initial IVA proposal will make you pay 100% of your disposable income into the IVA.

But over the course of the IVA, you might be able to keep some of your disposable income as long as it is within the additional income threshold.

What is the 10% rule for IVA?

Your additional income threshold is usually set at 10% more than what’s in your initial IVA proposal.

For example, if you usually earn £500 per week, but one week you worked some extra hours and earned £545, you would be allowed to keep the extra £45 because it’s within your 10% additional income threshold.

In this situation, you wouldn’t be forced to pay all of your disposable income into the IVA. You could instead spend the money on something other than essential living expenses, or you could save the money along with any other additional income you earn below the 10% threshold.

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

What happens if your income increases?

If your regular income increases due to a pay rise or a promotion, you must tell your IP immediately. Don’t wait for your next IVA review to disclose increased income.

Similarly, if you inherit money or come into money due to a windfall, you must also tell your IP immediately.

Your IP will then recalculate your regular income and adjust your monthly IVA payments so you pay more. It can work the other way as well if your income decreases. You might be able to get your IVA payments decreased.

What happens if you don’t tell your IP about higher income?

Failing to disclose an increase to your regular income to your Insolvency Practitioner is serious. You will have broken some of the conditions of your IVA, which could then result in the IVA failing.

What is the additional income threshold?

The additional income threshold is the amount of extra income you can earn without having to contribute it to your IVA. Once your IVA is approved and set up, your IP should tell you what your additional income threshold is.

You might get additional income by working overtime or receiving a bonus or commission from your employer. You might even start a second job.

Can I go on holiday while on IVA?

There’s nothing legally stopping you from physically going on holiday in the UK or abroad when you’re using an IVA. But you might not be able to go on holiday due to the cost.

You will be able to go on holiday while on an IVA if:

- The holiday was already fully paid for before the IVA started

- Someone else has offered to pay all of the expenses for you to go on holiday

- You have managed to save up additional income and use the money to pay for a holiday, which can be difficult and unlikely due to the significant expense of a holiday

Note, there is a big difference between someone offering to pay for your holiday, and someone offering to borrow you money to pay for your holiday. The latter can result in a failed IVA.

Can you get a loan while on an IVA?

There are usually restrictions that stop you from taking out any credit while on an IVA without getting written permission from your IP first. Sometimes you can apply for credit up to a small amount without getting IP permission.

However, it can be very difficult to get any amount of credit while using an IVA because lenders will consider you a high lending risk.

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Can you buy a car with an IVA?

You will only be able to purchase a car while on an IVA if you manage to save small amounts from any extra income accumulated within the additional income threshold. This could be impossible unless you buy a cheap car.

On top of this, your IVA might not factor in the costs of running a vehicle, including servicing and fuel costs. So getting a car is likely to be very difficult while on an IVA.

Can you get car finance with an IVA?

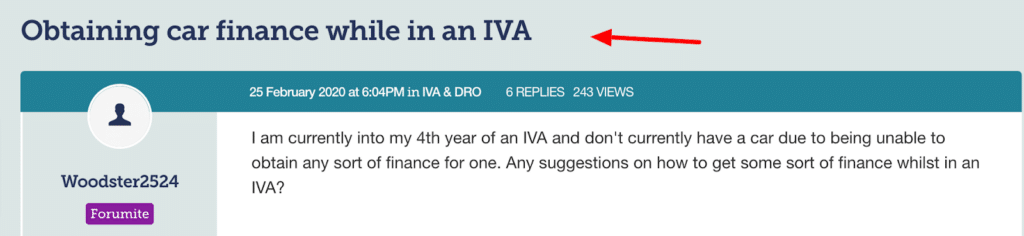

Because buying a vehicle outright is almost impossible on an IVA, many people ask whether it’s possible to get a vehicle on finance. Just like Woodster2524 asked on an online forum here:

Source: https://forums.moneysavingexpert.com/discussion/comment/76896681#Comment_76896681

The forum poster has been having difficulty getting approved for any type of finance to get a vehicle. This is quite common.

Many finance companies don’t accept people while they’re using an IVA. It can even be challenging to get a vehicle on finance immediately after an IVA due to a damaged credit record.

What is a failed IVA?

An IVA fails if you breach any of the conditions within your IVA agreement. The most common reason an IAV fails is when debtors don’t keep up with repayments. Another reason an IVA fails is when debtors conceal additional income from their IP.

When an IVA fails, your creditors can take court action against you to make you pay the debt. They can even petition to make you bankrupt. It’s best to avoid this situation. Speak with your IP if you’re struggling to keep up with payments.

IVA spending restrictions (Quick summary)

IVA spending restrictions can be summarised as:

- You will need to pay 100% of your regular disposable income into the IVA

- Thus, you will have to live on a strict budget without being able to make luxury purchases

- However, you can save a small amount of irregular additional income earned as long as it’s within your additional income threshold

- Keeping these smaller payments could help you save, or you could choose to spend the money as you wish

Alternative debt solutions

An IVA isn’t the only debt solution you may want to consider. There are other solutions that can also be effective at dealing with multiple creditors. Some other options will also help you write off some of the debt.

Learn more on my How to Get Out of Debt blog and speak to a debt charity for tailored debt advice.