Can I Sell a Car Which is on Finance?

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you wondering if you can sell your car that is on finance? You’re in the right place. Every month, over 12,000 people visit this site for advice on topics just like this one.

In this article, we’ll discuss:

- The different ways you can buy a car

- If you need to pay for a car on finance

- How to lower your repayments

- The good and bad points of a Hire Purchase Agreement

- How to sell a car on finance legally

We know that the thought of a debt can be worrying – you may be scared about not being able to pay or what might happen if you don’t pay.

You’re not alone. We’re here to help you understand how to handle your car finance and what you can do if you want to sell your car.

What car financing is available?

You could purchase a car on finance in several ways which I’ve listed below:

- Hire Purchase (HP) which is similar to taking out a mortgage but on a vehicle instead of a house

- Personal Leasing, otherwise known as contract hire

- Personal Contract Purchase (PCP)

- Personal Loan

- Credit card purchase – which can be incredibly expensive

All of the above allow you to buy a car on credit but some are expensive and restrictive ways of doing so. Especially when it comes to selling a financed car to buy a newer one.

What is a Hire Purchase Agreement?

Otherwise known as buying a car on HP, a Hire Purchase Agreement involves paying for it over several months or even years.

You pay a lump sum first and then monthly instalments to pay off the full amount with interest added every month! Once you’ve paid off the outstanding balance you own the vehicle.

It’s worth noting that HP Agreements are governed by the Financial Conduct Authority (FCA). It’s like taking out a mortgage on a car rather than a property!

What are the pros and cons of an HP Agreement?

The advantage of buying a car on HP includes:

- You own the car once you’ve paid off the outstanding balance

- There are usually no mileage restrictions

- The loan period tends to be flexible

The cons of buying a car on HP are:

- If you miss an instalment, the car could be repossessed

- When you miss a payment, it could impact your credit rating

- You can’t sell a car that you bought using a Hire Purchase Agreement until you’ve paid the full amount

So, if you bought the car on HP, you won’t be able to sell it until you’ve paid off the outstanding balance! Why? Because the Hire Purchase Company is the legal owner.

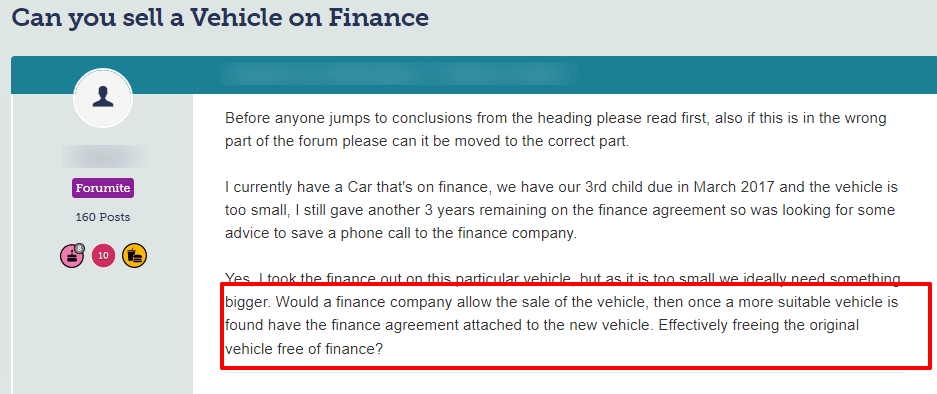

Check out what one person asked about selling a car on finance on a popular forum:

Source: Moneysavingexpert

You are the registered keeper, but not the actual owner when you purchase a car on HP.

However, you can pay off the outstanding hire purchase balance and then sell the car which is perfectly legal!

» TAKE ACTION NOW: Fill out the short debt form

What is Personal Leasing (contract hire)?

You could’ve leased the car which is similar to renting a property whether it’s a flat or house.

When you enter into a Personal Leasing agreement, you agree to pay a fixed monthly fee over an agreed leasing period.

But you’d have to pay a deposit which could be 3 to 6 times the monthly instalment which is an expensive way of doing things!

When a lease agreement comes to an end, you hand back the keys to the company that leased the vehicle to you. Moreover, you shouldn’t have to pay anything extra if the car’s in good condition when you return it.

However, if the vehicle is damaged or in bad condition, you’d have to pay extra!

The downside to taking a car on lease is that you can’t ever sell it! Not even when the lease agreement ends.

In short, you never own the car and if you try to sell it, you’d be breaking the law!

What is a Personal Contract Purchase (PCP)?

You may have purchased the car using a Personal Contract Purchase (PCP). It’s an option that many people use when they want to change a car every couple of years or so.

Moreover, it’s not a ‘loan’ that covers the full cost of a car. It’s a loan that covers the cost of the car’s value and its value at the end of the hire contract.

For example, if you enter into a PCP agreement that lasts three years and the cost is £10,000 and the car’s value is predicted to be £5,000 in three years, you’d pay:

- A deposit of £1,000 which is 10% of its initial value

- The loan amount owed would be £9,000

- Over three years, however, you’d pay £4,000 which factors in the predicted value of the car at the end of the agreement

However, you’d have to pay interest on the £9,000 when you enter into this type of agreement.

When you’ve paid the full outstanding amount, you can:

- Keep the car by paying the extra £5,000 which means you could sell it

- Return the car to the company

The downside is that you can’t sell a car you bought on finance using a PCP agreement. Not unless you pay off the full amount owing to the company that owns the car!

How a debt solution could help

Some debt solutions can:

- Stop nasty calls from creditors

- Freeze interest and charges

- Reduce your monthly

A few debt solutions can even result in writing off some of your debt.

Here’s an example:

Situation

| Monthly income | £2,504 |

| Monthly expenses | £2,345 |

| Total debt | £32,049 |

Monthly debt repayments

| Before | £587 |

| After | £158 |

£429 reduction in monthly payments

If you want to learn what debt solutions are available to you, click the button below to get started.

Did you buy the car using a personal loan?

If you purchased your car using a personal loan you took out with a bank or other financial institution, you own the vehicle from the outset.

There’s no lien placed on a car when you buy it using a personal loan!

In short, you’re the legal owner and the registered keeper of the car. However, if you decide to sell the car, you’d still have to make the monthly loan instalments to the lender.

Plus, there’ll be interest added to the outstanding balance.

The advantage of buying a car using a personal loan is you own it outright and you can sell the car when you want to. However, you’d still be liable for all the monthly payments until the outstanding balance is paid off.

Can you sell a car you bought using a Credit Card?

Buying a car using a credit card is just like purchasing anything else on credit. You pay the full amount upfront and then pay off the credit card in monthly instalments!

The interest incurred when you buy a car with a credit card could be prohibitive!

The only advantage is that when you use a credit card for any purchase, it provides you with a ton of consumer protection.

You can sell the car because there’s no lien on it when you buy it using a credit card. You own the vehicle outright.

However, you have to make monthly payments to the credit card company even when you sell the car! If you miss any payments, it’d harm your credit history and you could face dealing with a debt collection agency.

You could end up with a County Court Judgement registered on your credit report. A CCJ would make it hard for you to borrow money, get a credit card, bank loan or mortgage.

How do you find out if a car is on finance?

You can find out if a car is on finance by carrying out a Hire Purchase Investigation through the RAC, Greenflag and the AA.

I’ve listed how to do this below:

| RAC HPI check | https://www.rac.co.uk/buying-a-car/rac-car-data-check/ |

| AA car check | https://www.theaacarcheck.com/ |

| Greenflag vehicle check | https://vehiclecheck.greenflag.com/ |

So, can you sell a car with outstanding finance?

You can’t sell a car with outstanding finance on an HP agreement until you’ve paid for the car in full. You don’t own the car when you buy it using a Hire Purchase Agreement.

The car belongs to the Hire Purchase company!

Is it against the law to sell a car with finance?

Yes. If you sell a car which is still under finance, you’d be breaking the law. The ‘actual’ owners of the vehicle could be a dealer, Hire Purchase or finance company and they could take you to court.

So selling a vehicle which is still under finance to pay off some debts you might have, could end up making things much worse! It could seriously harm your financial situation.

What could happen if you sell a car still under finance?

You’d be pushing your luck if you sell a car that’s still under finance. As mentioned, the legal owner could start legal proceedings against you.

You could receive heavy financial penalties!

Worst still, the legal owner could repossess the car from the new owner! In short, you could face legal action from the person you sold the car to.

You could avoid court proceedings by giving back the money the new owner paid for the car! But if you’re struggling financially, you may not be able to.

Could you go to prison for selling a car on finance?

Not usually no. Selling a car which is still on finance won’t result in you being sent to prison because it’s a civil matter.

However, when you sell a car under finance to defraud an insurance provider, it could be deemed as ‘fraud’.

You could receive a custodial sentence!

It’s one of the reasons why most owners don’t sell cars which are still under finance. The risk of going to prison for fraud is too great even if you’re experiencing financial hardship!

What is an HPI check?

An HPI check lets you check whether a vehicle is on Hire Purchase. The HPI is short for Hire Purchase Investigation.

When you sell a vehicle, chances are the buyer will carry out an HPI check before parting with any money.

The check also establishes whether the car was written off in the past and whether it’d been seriously damaged.

If the results of an HPI check show a car has finance on it, the buyer won’t touch it!

» TAKE ACTION NOW: Fill out the short debt form

How can you legally sell a car on finance?

The only way to sell a car that’s on finance is to settle the amount owed and end the hire purchase agreement.

In short, you’d have to pay off the outstanding early if you want to sell it before the HP agreement ends. However, you’d need to check with the hire purchase company first to make sure they’ll accept an early settlement.

You may have to pay an ‘early settlement’ fee.

Also, you’d have a specific amount of time to pay the money that’s outstanding to the hire purchase company. Once it’s paid, you legally own the car and you can sell it.

There’s another catch to paying off a car that’s on hire purchase early. If the fees and interest make the settlement amount higher than what a car is worth, you could be left with negative equity!

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Reviews shown are for The Debt Advice Service.

Could you return the car instead of selling it?

Rather than trying to pay off a car on finance early so you can sell it, you should consider returning the vehicle to the hire purchase or finance company.

It’s worth considering if you’re struggling to keep up with payments and you’re experiencing financial hardship.

This is known as a ‘voluntary termination’, and it means you won’t get further into debt.

The proviso to returning a car on finance, however, is that you must have paid 50% of its value. That said, you may be allowed to pay the remaining amount in a finance arrangement to take you up to the 50% mark.

Also if you’ve repaid more than the 50%, it may not be possible to return the vehicle, unless the finance contract you signed includes a voluntary termination option.

Will returning a car on finance harm your credit rating?

Under the Consumer Credit Act, you can settle and terminate a Hire Purchase Agreement. That said, the termination will show on your credit file but it shouldn’t affect it.

Lastly, can you sell a car which is on finance?

You can’t sell a car that’s financed on a Hire Purchase Agreement because you’re not the legal owner.

You’re the registered keeper, but the Hire Purchase Company or finance company owns the vehicle!

If you try to sell it, chances are the purchase could check whether there’s any finance on the car. If the results are positive, they’ll likely decline to buy it.

Moreover, if you do sell a car that’s still on finance and the Hire Purchase Company or lender finds out, they could repossess the car.

The new owner could take you to court and you may face legal action from the HP company too!

In short, you can’t sell a car that’s on finance without first settling the amount owed on it. Once you’ve paid off the HP, you legally own the car and therefore, you can legally sell it!

Thanks for reading my post. I hope the information helps you decide what to do if you want to sell a car that’s still in finance!