Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Powered by MoneyNerd, featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried because Opos Limited Debt Collection contacted you? You might be feeling stressed about how to handle this.

If so, you are not alone. Each month, over 12,000 people visit this website to understand debt topics.

In this article, we’ll explain:

Who Opos Limited are, and why they might contact you

How to deal with Opos Limited

Ways to lower your repayments

Your rights when dealing with debt collectors

The consequences of not responding to Opos

We understand that dealing with debt collectors can be tough; some of our team members have been in your shoes.

Don’t worry; we’re here to help you understand how to deal with Opos Limited Debt Collection.

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Why would Opos contact you?

Opos may be chasing an outstanding debt for another company. Or the debt collector could be contacting you for a debt they purchased!

Maybe you defaulted on something, or you ignored a court order to pay a creditor. Whatever the reason, if a creditor asks Opos to recover the amount, they’ll contact you. And they can be pretty persistent!

Don’t panic when you get a letter from Opos because debt collectors are obligated to ‘prove’ the debt is yours! Moreover, debt collectors must follow the law when they contact you.

Opos could contact you by letter, phone or email. A field agent could visit you at home! However, when the debt collection agency contacts you, the first thing to do is stay calm.

It’s better to deal with the problem head-on. So, although stressful, it’s best to respond to Opos. If you prefer, you can write to them rather than speak to someone over the phone!

When writing to Opos, ask for ‘proof’ the debt is yours. Debt collectors are obliged to provide this information. A representative may ‘tell’ you they know the debt is yours, but that’s not good enough!

Opos must produce an authenticated copy of an agreement you entered into. A debt can’t be enforced if they can’t produce the evidence!

Seek advice from one of the debt charities if you’re confused or have any doubts about the way Opos contacts you. Their advice could be invaluable when dealing with a debt collector!

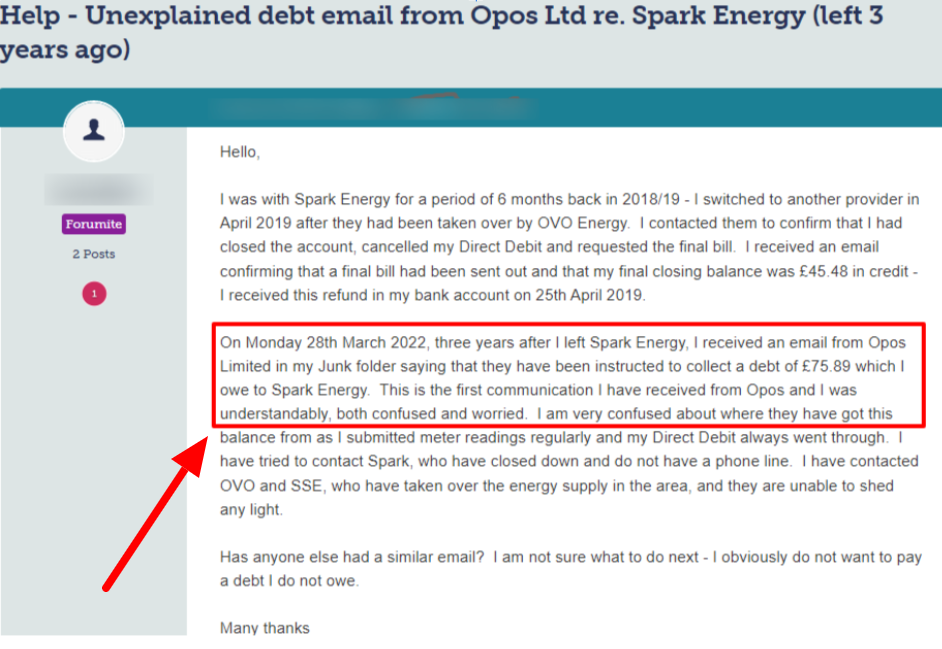

Check out what happened to one very unfortunate person who received a letter from Opos:

Opos could report you to credit bureaus if you ignore their correspondence. It would ruin your credit rating. Moreover, the amount owed could increase so it’s even harder to get back on track!

What happens when you don’t respond to Opos?

Opos could start legal proceedings against you. Moreover, the problem starts to escalate if you don’t respond to the debt collector’s letters. It could lead to:

So, in short, not responding to Opos correspondence could lead to more stress!

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

Debt collection agencies are highly regulated. Not only by the FCA but also by the Credit Service Association (CSA). Opos must follow the Code of Practice and if they don’t you can report them.

So for example, Opos cannot do the following:

Call you at unreasonable or unsociable times when you’ve asked them to call you at specific times

Contact you in ways you’ve asked them not to contact you

Call you at work

Take payment from you without your permission

Refuse to let you think about your options

Discuss a debt with other people which is a breach of your privacy

Pressure you to take out another loan to pay the debt they’re chasing you for

Use confusing legal jargon

Can you get out of paying Opos?

You could get out of paying Opos for two reasons which I’ve listed here:

The debt is six-plus years old and therefore unenforceable because it’s statute barred

Opos can’t prove the debt is yours!

However, for a debt to be statute barred it must meet certain criteria which are:

You never admitted liability

You haven’t paid anything towards the debt in the last six years

There’s no current court order or proceedings relevant to the debt

Can you stop Opos from contacting you?

Opos has the right to contact you but debt collectors cannot harass you with continuous calls/messages. You can write to Opos asking them to stop calling you at unsociable hours.

In short, you can tell Opos to contact you at specific times of the day. You can also dictate how debt collectors contact you. So, if you prefer to be contacted in writing, let them know.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.