Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Powered by MoneyNerd, featured in...

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.

Are you worried about dealing with IMFS Debt Collection? It can be a big worry when they get in touch. You might be feeling unsure about your rights or about how to handle the situation.

You’re not alone. Each month, over 12,000 people visit this site for advice on debt troubles.

In this article, we’ll cover:

Who IMFS Debt Collection is, and if they are real

If you have to pay IMFS Debt Collection

How you can lower your repayments to them

What to do when IMFS contacts you

What can happen if you don’t pay IMFS Debt Collectors

We understand how hard it can be when dealing with debt collectors; our team has been there too. That’s why we’re here to help you.

Ready to find out what you can do if you’re dealing with IMFS Debt Collection? Let’s get started!

Could you legally write off some debt?

There are several debt solutions in the UK, choosing the right one for you could write off some of your unaffordable debt, but the wrong one may be expensive and drawn out.

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

What should you do when IMFS contacts you?

It’s natural to panic when you get a debt collector’s letter drops through the letterbox, whether you’re aware of a debt or not! That said, the onus is on IMFS to prove the debt is yours!

So, the first thing to do when you get a letter from them is to ask them to ‘prove’ the debt is yours! Make sure you send the letter by registered post and keep a copy for your own records.

Debt collectors must respect your request. Moreover, don’t accept a ‘verbal’ affirmation that the debt is yours. IMFS must send you authenticated written proof!

If IMFS can’t prove the debt – they can’t make you pay it!

What happens when you don’t pay IMFS Debt Collectors?

IMFS has the right to escalate things when you don’t pay them. So, after their initial threatening correspondence, they could start legal proceedings to recover the debt.

When you don’t pay IMFS, they could:

Report you to credit bureaus which will impact your credit history

Apply for a court judgement to be issued. A CCJ will negatively impact your credit rating making it hard to borrow money

Apply to the courts for a Charging Order on your property although this is quite rare

What can IMFS Debt Collection legally do?

There’s a Code of Practice that all debt collection agencies must follow when they contact you. If IMFS fails to abide by the rules and regulations set out by the Credit Services Association and the FCA, you could report them.

Moreover, their actions may get you off the hook!

That said, debt collectors can legally:

Contact you and visit you at home

Ask you to pay them directly

Discuss a debt with you discreetly and politely

However, debt collectors would be acting unlawfully if they:

Force their way into your home

Clamp your vehicle

Seize your possessions

Use documents that appear to be court-issued when they’re not

Pretend they have the same powers as Enforcement Agents (bailiffs) which is a criminal offence

Talk to your neighbours, friends, family or employer about your alleged debt which breaches privacy laws

Use legal jargon to deliberately confuse you

Force you to take out more credit to pay the debt

Thousands have already tackled their debt

Every day our partners, The Debt Advice Service, help people find out whether they can lower their repayments and finally tackle or write off some of their debt.

Natasha

I’d recommend this firm to anyone struggling with debt – my mind has been put to rest, all is getting sorted.

No. The chances are IMFS Debt Collection probably won’t give up chasing you for payment. Debt collectors are persistent and will escalate things when you ignore them!

So, rather than bin a letter from IMFS, contact them in writing and insist:

They produce authenticated proof the debt is you

Only contact you at specific times and in chosen ways

Debt collectors must respect these requests and if they don’t, file a complaint against them. First with their head office. Second with the Financial Ombudsman Services!

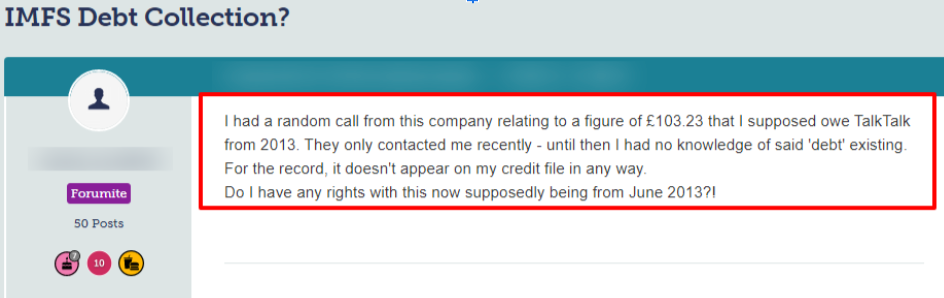

Check out what one person had to deal with when contacted by IMFS:

4100 Park Approach, Thorpe Park, Leeds, West Yorkshire, England, LS15 8GB

Could you legally write off some debt?

Answer below to get started.

This isn’t a full fact find. MoneyNerd doesn’t give advice. We work with The Debt Advice Service who provide information about your options.

Did you like this article?

Show your support ❤️

We're glad you liked the article! As a small team, your support means everything to us. If you could rate us on Google, it would be amazing. Thank you!

Could you legally write off some debt? Answer below to get started.

For free & impartial money advice you can visit MoneyHelper. We work with The Debt Advice Service who provide information about your options. This isn’t a full fact-find, some debt solutions may not be suitable in all circumstances, ongoing fees might apply & your credit rating may be affected.